How To Survive On One Income When You Become A Stay At Home Mom

Welcome to Your New Season, Mama

Oh, sweet mama, I see you. You are standing at the threshold of one of the most beautiful, transformative, and—let’s be honest—daunting transitions of your life. The decision to stay home with your little one is a choice made of pure love and a desire to be the primary witness to every giggle, crawl, and milestone. But as a doula and a sister who has walked this path, I know that the ‘financial nesting’ phase can feel just as intense as the physical nesting phase. Moving from two incomes to one isn’t just about the numbers on a spreadsheet; it’s about a shift in identity, a restructuring of your daily rhythm, and a new way of viewing your family’s resources. You might be feeling a mix of excitement and a little bit of ‘how are we actually going to do this?’ fear. Take a deep breath. Just as your body was designed to birth and nourish your baby, your family is capable of adapting to this new financial landscape. We are going to walk through this together, step by step, with practical tools and a whole lot of heart. We aren’t just talking about surviving; we are talking about creating a life where your family thrives on less, so you can experience more of what truly matters.

The Financial Heart-to-Heart: Aligning Your Values

Before we even touch a calculator, we need to talk about the ‘why.’ In my work as a doula, I always tell my clients that a clear vision is the best tool for labor. The same applies to your finances. You and your partner need to be on the exact same page. This isn’t just about ‘cutting back’; it’s about choosing what you value most. Sit down together—perhaps after the little one is asleep—and have a gentle, honest conversation about your priorities. What are the non-negotiables for your family’s peace of mind? Is it organic food? Is it a certain amount of savings for emergencies? Is it being able to afford that one weekly playgroup? When you align your spending with your values, the ‘sacrifices’ don’t feel like losses; they feel like intentional choices.

“Our budget is not a restriction; it is a reflection of our family’s deepest priorities and our commitment to being present for our children.”

To start this process, I recommend a deep-dive audit of your current spending. You need to know exactly where every dollar is going before you can redirect it. Use the table below to categorize your current lifestyle and identify where the ‘leaks’ might be.

| Expense Category | The ‘Two-Income’ Habit | The ‘SAHM’ Shift |

|---|---|---|

| Dining & Food | Frequent takeout and $7 lattes. | Meal planning and bulk ‘nesting’ prep. |

| Entertainment | Subscription overload and movie nights out. | Library passes and community park dates. |

| Impulse Buys | Target ‘dollar spot’ runs and Amazon hauls. | The 48-hour wait rule for all non-essentials. |

| Transportation | Two commuting vehicles and high gas costs. | Consolidating errands and potentially selling a car. |

Mastering the ‘Dry Run’ Before the Big Transition

If you are still pregnant or currently on maternity leave, the best thing you can do is a ‘dry run.’ For at least three to six months before you officially leave your job, try living entirely on your partner’s income. This is the ultimate ‘financial labor rehearsal.’ Take your entire second paycheck and move it immediately into a high-yield savings account. Do not touch it. This serves two vital purposes: it builds a robust ‘cushion’ (your postpartum peace-of-mind fund), and it proves to you that you can survive on the remaining income.

Steps for a Successful Financial Rehearsal

- Automate Your Savings: Set your payroll to deposit your check directly into a separate account so you never even ‘see’ the money.

- Track Every Penny: For 30 days, write down every single purchase. You will be amazed at how much ‘phantom spending’ occurs on things like convenience snacks or unused apps.

- Identify Your ‘Safety Number’: Determine the absolute minimum your family needs to cover housing, utilities, and basic food. Everything else is a ‘variable’ that can be adjusted.

During this phase, pay close attention to your emotions. If you feel panicked, look at the numbers again. If you feel empowered, lean into that feeling! This is your time to adjust the ‘dosage’ of your spending before the stakes are higher.

Slashing the ‘Big Three’: Housing, Food, and Transport

To truly thrive on one income, we have to look at the ‘Big Three’ expenses. These are the areas where you can find the most significant savings. As a doula, I’m all about nourishing the mother, and that starts in the kitchen. Food is often the largest variable expense for families. By moving away from convenience and toward ‘slow food,’ you save thousands of dollars a year. This doesn’t mean you have to spend all day over a stove; it means becoming a master of the slow cooker and the bulk-buy aisle.

The Art of the Frugal, Nourishing Kitchen

- Bulk Buying Staples: Rice, beans, oats, and frozen vegetables are your best friends. They are nutrient-dense and incredibly cheap when bought in large quantities.

- The ‘Meal Theme’ Strategy: Reduce decision fatigue and food waste by having set themes (e.g., Meatless Monday, Taco Tuesday, Soup Sunday).

- Generic over Brand: Most store-brand staples are identical in quality to name brands but cost 30% to 50% less.

| High-Cost Item | The Frugal Swap | Estimated Monthly Saving |

|---|---|---|

| Pre-cut fruit/veg | Whole produce (cut it yourself) | $40 – $60 |

| Individual snack packs | Bulk bags and reusable containers | $25 – $40 |

| Premium Coffee Shop | Home-brewed with a nice frother | $80 – $150 |

| Paper Towels/Napkins | Reusable cloth rags and napkins | $15 – $25 |

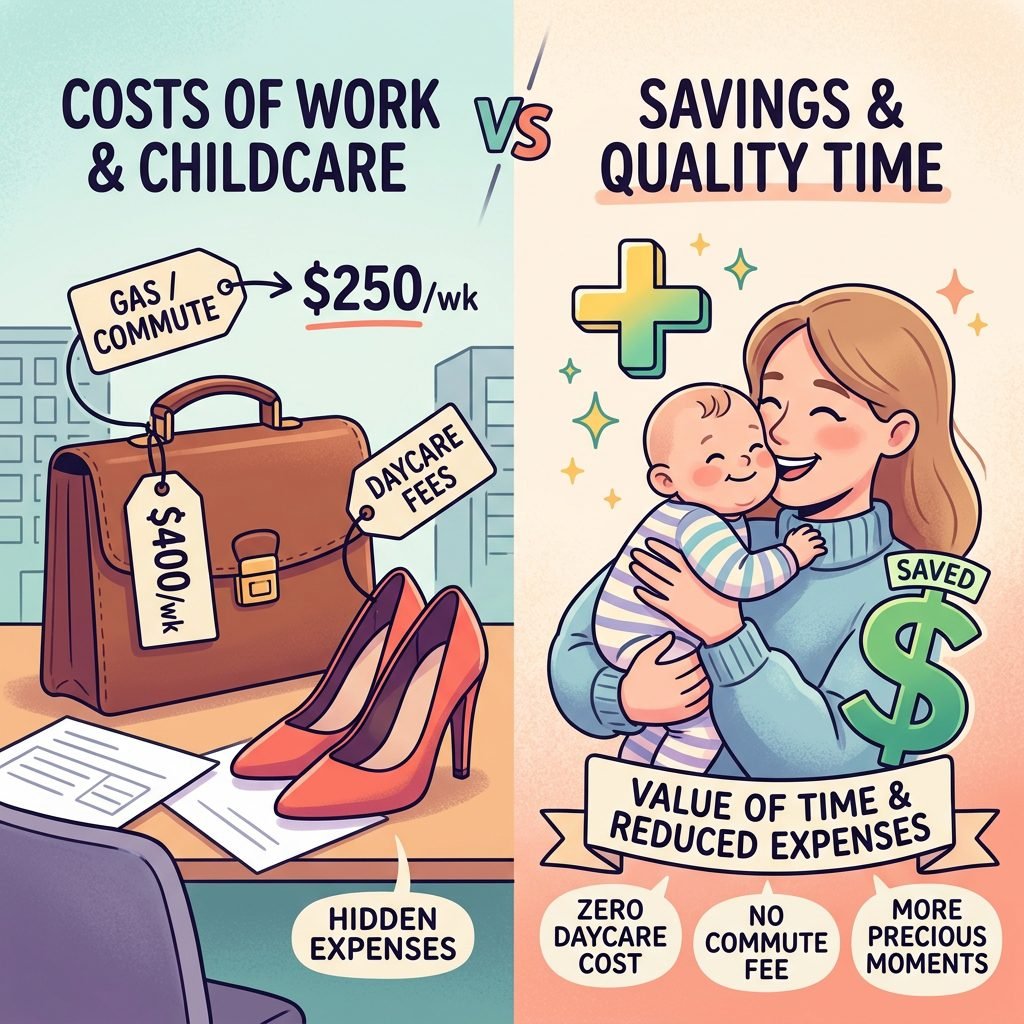

The Hidden Math: What You Save by Not Working

Mama, I want you to take a moment and calculate the real cost of your job. Often, when we look at our salary, we forget to subtract all the expenses required to earn that salary. When you become a stay-at-home mom, many of these costs simply vanish. This realization can be incredibly liberating and can help bridge the gap between your previous two-income life and your current one.

The ‘Work-Related’ Expense Audit

- Childcare: This is usually the biggest one. Calculate the monthly cost of daycare or a nanny.

- Commuting: Gas, tolls, parking, and the extra wear and tear (and insurance) on your vehicle.

- Work Wardrobe: Professional clothing, dry cleaning, and makeup.

- Convenience Costs: The ‘I’m too tired to cook’ takeout, the morning latte, and the office birthday gifts.

Often, after subtracting these costs and accounting for the lower tax bracket your family might fall into, the ‘loss’ of income is significantly less than it appears on paper. You aren’t just ‘losing’ a paycheck; you are ‘gaining’ the value of your own labor in the home.

“I am not just ‘staying home’; I am managing the most important organization in the world—my family’s well-being and our home’s economy.”

Creative Income Streams and The ‘Gentle’ Side Hustle

Sometimes, the budget still feels a little tight, and that’s okay. Many stay-at-home moms find that a ‘gentle side hustle’ provides just enough ‘fun money’ or ‘buffer money’ without taking away from their primary role. The key here is sustainability. You don’t want a second job that leaves you burned out for your baby. Look for things that utilize skills you already have or that can be done during nap times.

Low-Stress Income Ideas for SAHMs

- Digital Freelancing: If you have skills in writing, graphic design, or bookkeeping, platforms like Upwork or specialized agencies can offer flexible projects.

- Selling the ‘Clutter’: As you organize your nursery and home, sell items you no longer need on Facebook Marketplace or Poshmark. This is a great way to fund new baby gear.

- Virtual Assistant Work: Many small business owners need help with emails or social media for just 5-10 hours a week.

- Teaching or Tutoring: If you have a background in education or a specific craft, online tutoring or creating a small digital course can be very lucrative.

Remember, your primary ‘job’ right now is recovery and bonding. Do not feel pressured to start a business in the first six months postpartum. Give yourself grace, mama.

The Emotional Landscape: Navigating Financial Dependency

We need to talk about the ‘money talk’ in your relationship. For many women who have always been financially independent, moving to a single income can trigger feelings of guilt or a sense of ‘asking for permission’ to spend money. This is a major hurdle that can lead to resentment if not addressed. You are a full partner in this family. Your contribution to the home—the childcare, the cooking, the emotional labor, the management—has immense economic value.

Communication Scripts for Financial Peace

“I’ve been feeling a little anxious about our spending lately. Can we sit down on Sunday and look at the budget together so I feel more confident about our plan?”

“I would like us to have a ‘no-questions-asked’ personal allowance for both of us each month. It helps me feel like I still have some autonomy over my personal needs.”

Establishing an ‘allowance’ for both partners—even if it’s just $20 or $50 a month—is a game-changer. It removes the need to ‘check-in’ for small personal purchases and maintains a sense of individual agency. You are a team, and the money coming into the house is ‘our’ money, not ‘his’ money. Keeping this mindset is essential for your mental health and the health of your marriage.

Conclusion

You Are Richer Than You Think

As we wrap up this guide, I want you to remember that wealth isn’t just about the balance in your checking account. You are building a legacy of presence, a home filled with the scent of home-cooked meals, and a childhood for your little one that is anchored by your constant, loving presence. Surviving on one income is a skill that you will master over time, just like you mastered diaper changes and soothing a colicky baby. There will be months where the budget is tight, and there will be months where you feel like a financial wizard. Through it all, keep your eyes on the prize: the freedom to be exactly where you want to be. You’ve got this, mama. You are resourceful, you are capable, and you are doing something incredibly brave and beautiful for your family. Welcome home.