Stop Overpaying! How to Negotiate Your Hospital Bill After Birth

Welcome to the fourth trimester, mama. You have just achieved the extraordinary—you brought a beautiful new life into this world. Right now, your days (and nights) should be completely focused on skin-to-skin snuggles, mastering the perfect swaddle, establishing your feeding journey, and allowing your incredible body to heal. But then, usually right around the time you are navigating your first major sleep regression, it arrives in the mail: the hospital bill.

As a doula and maternal care expert, I have sat with countless weeping mothers who felt completely blindsided by a piece of paper demanding thousands of dollars. The sheer panic of seeing a five-figure balance after insurance adjustments is enough to spike anyone’s postpartum anxiety. But take a deep, cleansing breath with me right now. Lower your shoulders. Relax your jaw. You do not have to pay that terrifying number immediately, and more importantly, you likely do not have to pay that exact amount at all.

Hospital billing is notoriously messy, complicated, and prone to massive errors. When you are in active labor, you are not tracking every Tylenol given, every specialist who pops their head into your room, or whether your baby briefly visited the nursery. The hospital’s billing department relies on automated codes, and mistakes happen constantly. In this sisterly, step-by-step guide, we are going to put on our financial advocacy hats. I am going to walk you through exactly how to audit your birth bill, the precise scripts to use on the phone, and the legal protections you have to ensure you stop overpaying and keep your family’s hard-earned money where it belongs.

The Postpartum Financial Shock: Why Your Bill is Probably Wrong

First, let me validate exactly what you are feeling: it is profoundly unfair that you are expected to navigate complex medical billing while wearing mesh panties and operating on two hours of fragmented sleep. The American healthcare system does not hand out instruction manuals for new parents, but as your virtual doula, I am here to give you the inside scoop.

It is estimated that up to 80% of hospital bills contain errors. Let that sink in. Eight out of ten families are being overcharged. When you give birth, multiple different entities are billing you simultaneously. You might receive separate bills from the hospital facility, the anesthesiologist (who gave you your epidural), the obstetrician or midwife, the pediatrician who examined your baby, and the laboratory that ran your bloodwork. It is a chaotic web of paperwork.

Common Reasons for Inflated Birth Bills

- Upcoding: This happens when a hospital bills for a more expensive service than you actually received. For example, billing for a complex Level 5 emergency room visit when you simply arrived in active labor and were immediately wheeled to labor and delivery.

- Double Billing: Being charged twice for the same medication, the same ultrasound, or the same set of postpartum vitals.

- Canceled Services: You may have requested a lactation consultant, but she never showed up—yet the charge still mysteriously appears on your statement.

- The “Skin-to-Skin” Charge: Yes, some hospitals genuinely try to charge a fee for placing your own baby on your chest in the operating room after a C-section, often coded as “activation of the surgical team.”

Your very first step when you receive that terrifying summary bill is to put it in a folder and remember this golden rule: Never pay a summary bill without investigating it first. You have time. Medical debt does not instantly go to collections, and you have significant legal rights.

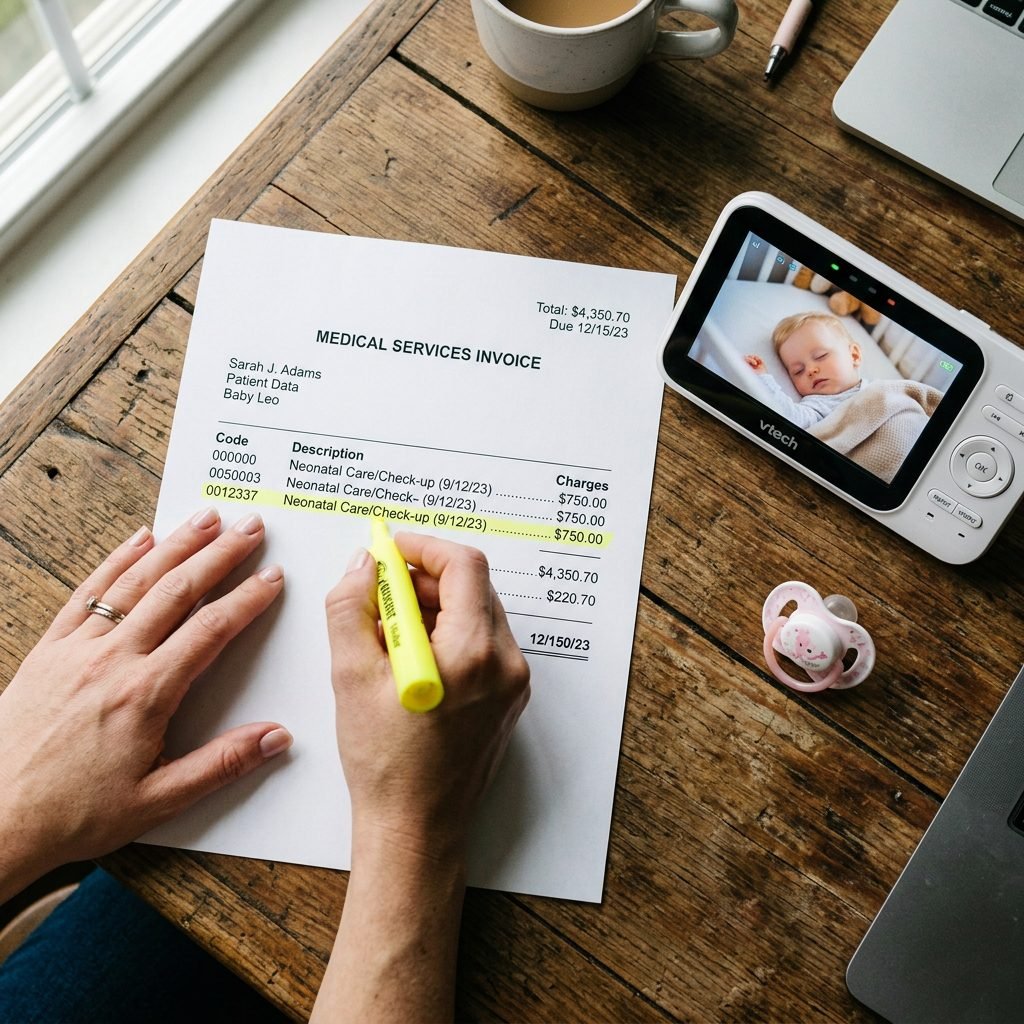

Step 1: Requesting the Elusive “Itemized Bill”

When the hospital sends you a bill, it usually looks like a simple summary. It will say something vague like “Pharmacy: $1,200” or “Room and Board: $4,500.” This summary is practically useless for our purposes. You cannot dispute a charge if you do not know what the charge actually is.

To uncover the truth, you must demand an itemized bill with CPT codes. CPT stands for Current Procedural Terminology. These are the universally recognized five-digit codes that medical providers use to communicate with insurance companies. An itemized bill will break down every single band-aid, ibuprofen, IV bag, and minute of nursery time you are being charged for.

How to Ask for Your Itemized Bill

Grab a notebook, make yourself a warm cup of lactation tea or coffee, and call the billing department number listed on your statement. Here is exactly what you should say:

“Hi, my name is [Your Name] and my account number is [Account Number]. I am calling regarding my recent labor and delivery bill. Before I can process any payment, I need you to mail and email me a completely itemized bill that includes all CPT codes for every charge. I also need my account placed on a 30-day billing hold while I review these documents.”

Do not let them rush you. Legally, they must provide this document. By asking for a 30-day billing hold, you are pausing the clock, ensuring the hospital will not send your account to a collections agency while you do your homework.

Step 2: How to Audit Your Birth Bill Like a Pro

Once that multi-page itemized bill arrives, it is time to grab a highlighter. I want you to sit down with your partner or a trusted friend—do not do this alone if you are feeling emotionally fragile—and go line by line. You are looking for anything that does not match your memory of your birth experience.

The Postpartum Bill Audit Checklist

- Nursery Fees: If your hospital was “baby-friendly” and your infant stayed in your room in a bassinet for your entire stay, you should not be charged a daily nursery fee. Cross it out.

- Medication Quantities: Did they charge you for 20 ibuprofen pills when you only took 4? Did they charge you for an IV drip that was ordered but never actually hooked up to your arm?

- Lactation and Specialist Fees: Did a lactation consultant actually spend 30 minutes helping you latch, or did a nurse just hand you a pamphlet? If it was the latter, dispute the specialist charge.

- Time of Discharge: Check the exact time you were discharged. Hospitals sometimes charge for an extra full day of room and board if you leave past a certain hour, even if you were just waiting on the doctor to sign your paperwork.

To help you organize your thoughts, use this quick reference table of the most common delivery room billing errors and how to handle them.

| Error Type | What It Looks Like on the Bill | How to Dispute It |

|---|---|---|

| Routine Supply Markups | “Postpartum Kit” or “Mucus Extractor” | Ask if these are considered “routine supplies” that should be bundled into the room rate. |

| Phantom Nursery Fees | “Level 1 Nursery” or “Infant Room/Board” | State clearly: “My baby roomed-in with me 100% of the time. Remove this facility charge.” |

| Unused Medications | Multiple charges for “Oxytocin” or “Epidural Anesthesia” | Request cross-referencing with your medical chart to prove what was actually administered. |

| Out-of-Network Surprises | Separate bill from an out-of-network Anesthesiologist | Invoke the No Surprises Act if you delivered at an in-network facility. |

Step 3: Unlocking Financial Assistance and Self-Pay Discounts

Here is a massive, well-kept secret of the healthcare industry: If you delivered at a non-profit hospital (and more than half of US hospitals are non-profit), they are legally required by the IRS to offer a Financial Assistance Policy (FAP), often referred to as “Charity Care.”

Many families assume they make too much money to qualify for financial assistance. This is a huge misconception! Depending on the hospital and the cost of living in your state, families making up to 400% of the federal poverty level can qualify for heavily discounted or completely forgiven bills. For a family of three or four, this can mean earning upwards of $90,000 to $120,000 a year and still qualifying for a massive reduction in your bill.

How to Apply for Charity Care

Go to your hospital’s website and search for “Financial Assistance Application” or “Charity Care Policy.” You will need to submit proof of income (like recent pay stubs or your last tax return) and a brief letter explaining your situation. While they process your application, your bill goes on hold.

The “Self-Pay” or “Cash Pay” Discount

If you are uninsured, or if you have a massive high-deductible plan and are paying entirely out of pocket, you should never pay the “chargemaster” rate (the hyper-inflated sticker price). Hospitals routinely offer a 20% to 50% discount for patients who pay in cash. Why? Because it saves them the administrative nightmare of fighting with insurance companies. If you have the funds to pay a lump sum, always call and ask for the cash-pay discount.

Step 4: Scripts for Success – Exactly What to Say on the Phone

Negotiating can feel incredibly intimidating, especially when your hormones are fluctuating and you are running on empty. The key is to remove the emotion from the conversation. The billing representative on the other end of the line is just a person doing their job. Be unfailingly polite, but absolutely firm. Treat this like a business transaction, because that is exactly what it is.

Here are three copy-paste scripts you can use depending on your situation. Read them out loud a few times before you dial, and keep them right in front of you during the call.

Script for Disputing Inaccurate Charges

“Hello, I am reviewing my itemized bill from my delivery on [Date]. I am looking at CPT code [Insert Code] for [Insert Service/Medication]. After reviewing my medical records and birth plan, I can confirm I did not receive this service. I need this charge investigated and removed from my account, and I need an updated statement sent to me once the correction is made.”

Script for Negotiating a Lump-Sum Settlement

“Hi, I am calling about my balance of [Insert Total Amount]. This amount is a severe financial hardship for our growing family. I am prepared to offer a one-time, lump-sum payment of [Insert 40-50% of the total] today to settle this account in full. Can you authorize this settlement, or do I need to speak with a billing supervisor?”

Script for Requesting a Zero-Interest Payment Plan

“Hello, I am calling to set up a payment plan for my balance. I cannot afford the monthly minimum you have listed. According to my family’s budget, I can commit to paying [Insert affordable amount, e.g., $50] per month. I need to set up a 0% interest payment plan for this amount. Please confirm that this will keep my account in good standing and prevent it from going to collections.”

Protecting Your Credit and Knowing Your Rights

If the hospital is pushing back and refusing to negotiate, do not panic. First, it is crucial to understand the No Surprises Act, which went into effect on January 1, 2022. This federal law protects you from unexpected out-of-network bills. If you gave birth at an in-network hospital, but an out-of-network anesthesiologist or neonatologist treated you, they cannot legally send you a massive surprise bill. You are only responsible for your in-network cost-sharing amounts.

Medical Debt and Your Credit Score

Many new parents are terrified that an unpaid hospital bill will instantly destroy their credit score, preventing them from buying a house or a new family car. Take a deep breath, because the laws have recently changed heavily in favor of consumers:

- The One-Year Grace Period: Medical debt cannot be reported to the major credit bureaus (Equifax, Experian, TransUnion) until it is at least 365 days past due. You have a full year to negotiate, dispute, or set up a payment plan before your credit is ever touched.

- Debts Under $500: As of 2023, unpaid medical debts under $500 will no longer appear on your credit reports at all.

- Paid Medical Debt: Once a medical debt is paid off, it is immediately removed from your credit history (unlike credit card debt, which lingers for seven years).

If you set up a payment plan with the hospital—even if it is just $20 a month—as long as you make that payment consistently, the hospital will not send the account to collections. Never put a medical bill on a high-interest credit card just to make it go away. The hospital is essentially a 0% interest lender if you negotiate correctly.

Conclusion

Sweet mama, you have just accomplished a miracle. Your body grew, nourished, and birthed a human being. Dealing with aggressive hospital billing is the absolute last thing you should have to worry about during your postpartum recovery, but you are strong, capable, and entirely equipped to handle this. By asking for that itemized bill, auditing the charges, applying for financial assistance, and using the scripts provided, you are taking back your power and protecting your family’s future.

Remember, this process is a marathon, not a sprint. Take it one phone call at a time. Reward yourself with newborn snuggles and grace after every step. You do not have to accept the first number they give you. Stand your ground, use your voice, and know that you are doing an incredible job navigating the chaotic, beautiful, and sometimes exhausting journey of modern motherhood.