Why a Will Isn’t Enough: Setting Up a Revocable Trust Before Baby Arrives

Welcome to the Ultimate Financial Nesting Guide

Mama, I see you. You’re currently in the thick of choosing the perfect non-toxic crib mattress, washing those tiny organic onesies, and perhaps even practicing your breathing for the big day. It is a beautiful, busy time. But as your sister-in-spirit and your doula for all things ‘life-prep,’ I want to talk about a different kind of nesting: financial nesting. We often talk about birth plans, but we rarely talk about legacy plans.

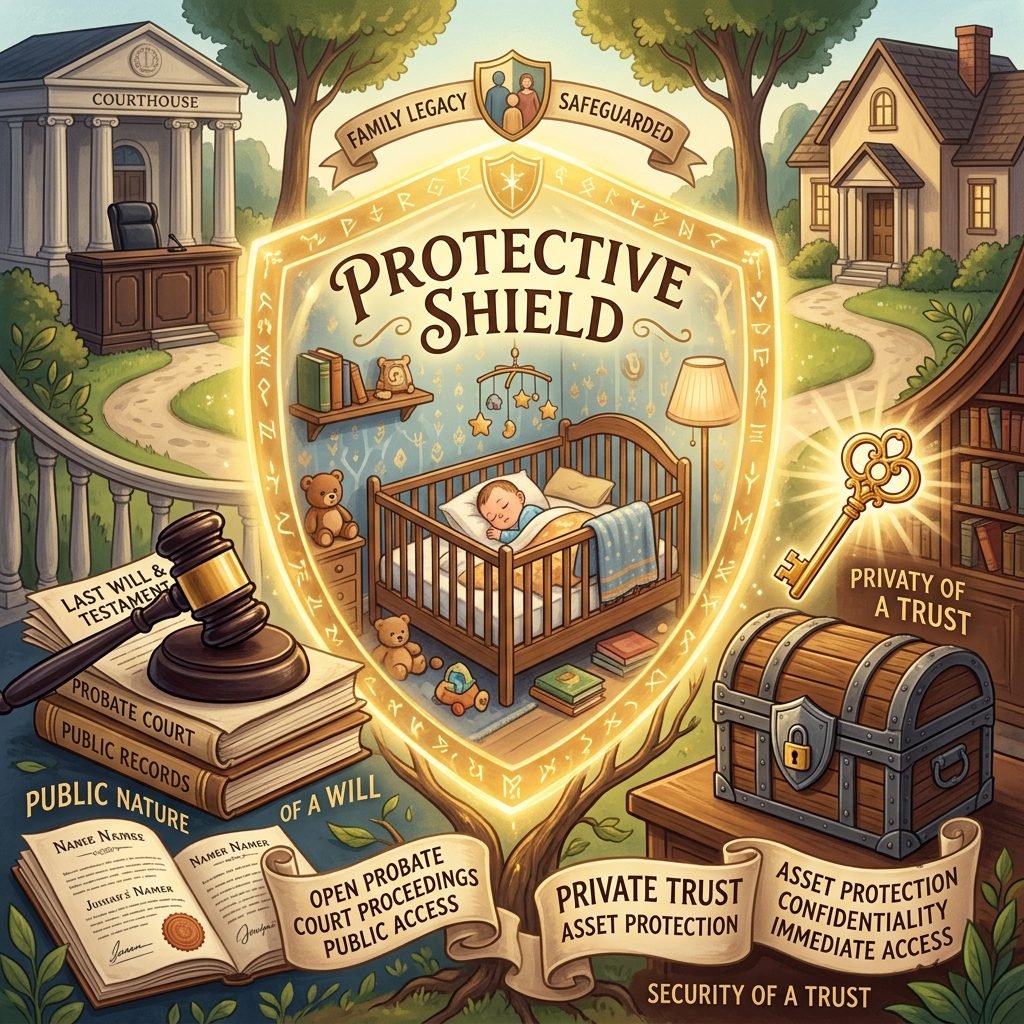

Most of us are told that once we have a baby, we simply need a ‘will.’ It’s on every Pinterest checklist. But here is the professional truth: for many families, a will is just the bare minimum. It’s like having a car with no insurance—it gets you there, but if something goes wrong, the cleanup is messy, expensive, and public. A Revocable Living Trust is the gold standard for protecting your little one. It ensures that if the unthinkable happens, your baby is cared for immediately, privately, and exactly how you envisioned, without a judge having to sign off on every diaper change or college tuition payment.

Will vs. Trust: Understanding the Protective Shield

Think of a will as a letter to a judge. It tells the court what you want to happen, but the court still has to oversee the entire process through a legal stage called probate. This can take months, or even years, and costs a significant percentage of your estate in legal fees. A Revocable Living Trust, however, is like a sturdy, private vault. You own the vault while you’re here, and the moment you aren’t, your handpicked ‘successor trustee’ takes the keys and continues managing things for your baby without ever stepping foot in a courtroom.

| Feature | Last Will and Testament | Revocable Living Trust |

|---|---|---|

| Probate Court | Required (Public and slow) | Avoided (Private and fast) |

| Control of Assets | Lump sum at age 18 (usually) | Staggered distributions (e.g., ages 25, 30) |

| Privacy | Public record | Completely private |

| Cost | Cheaper upfront, expensive later | More expensive upfront, saves thousands later |

| Immediate Access | Delayed by court approval | Instant access for guardian/trustee |

When we look at this comparison, the choice for a new mother becomes clear. We want speed and privacy for our children. We don’t want our family’s financial business published in local records, and we certainly don’t want a grieving guardian to wait six months for a court order just to pay for the baby’s daycare.

The Power of the ‘Staggered Inheritance’

One of the scariest parts of a simple will is that, in many states, if you pass away, your child receives their entire inheritance the moment they turn 18. Mama, let’s be real: did you have the financial maturity at 18 to manage a house, a life insurance payout, and a retirement fund? Most of us didn’t.

A Revocable Trust allows you to be a ‘parent from beyond.’ You can set specific milestones for when your child receives their money. This ensures they have enough for their needs while they are young, but doesn’t hand them a ‘lottery win’ before they’ve learned how to manage a budget.

Common Distribution Strategies:

- Health, Education, Maintenance, and Support (HEMS): The trustee can always use the money for the baby’s medical bills, private school, or basic living needs.

- The 25/30/35 Rule: Give them 1/3 of the principal at age 25, another 1/3 at 30, and the remainder at 35.

- Incentive Clauses: You can even stipulate that they receive a certain amount upon graduating college or starting a business.

“A trust isn’t about lack of trust in your child; it’s about providing a safety net that grows with them as they mature.”

Choosing Your ‘Village’: Guardians vs. Trustees

This is the part that makes most moms-to-be teary-eyed, but it is the most important ‘doula’ work we can do. You need to pick two different roles, and they don’t have to be the same person.

- The Guardian: This is the person who will kiss the boo-boos, help with homework, and raise your child in their home. They provide the emotional and physical care.

- The Trustee: This is the person who manages the money. They make sure the mortgage is paid, the college fund is invested, and the guardian has what they need to care for the child.

Sometimes, your sister is the perfect guardian but terrible with a checkbook. By using a trust, you can name your sister as the guardian and perhaps a financially savvy aunt or a professional entity as the trustee. This creates a system of checks and balances that protects your child’s inheritance from being mismanaged.

Script for Asking a Potential Guardian:

“Hey [Name], we’ve been doing some deep nesting lately and thinking about the future. We love the way you [mention a quality, e.g., value family/handle challenges], and it would give us so much peace of mind to know that if anything ever happened to us, you would be the one to raise [Baby’s Name]. We’ve set up a trust so you’d never have to worry about the financial side of things—that’s all handled. Would you be open to being named as the guardian?”

The ‘Funding’ Step: Don’t Leave the Vault Empty

This is the most common mistake parents make. They pay an attorney to create a beautiful trust document, put it in a fancy binder, and then… nothing. A trust is like a moving truck; if you don’t put your furniture inside it, the truck is useless.

Funding is the process of changing the titles on your assets from your name to the name of your trust. If your house is still in ‘Jane and John Doe’s’ name, it will still go to probate. It needs to be in ‘The Doe Family Trust.’

A Checklist for Funding Your Trust:

- Real Estate: File a new deed transferring your home to the trust.

- Bank Accounts: Visit your bank and update your checking and savings accounts to the trust’s name.

- Life Insurance: Update your beneficiary to be the trust, not the individual child (this prevents the 18-year-old lump sum issue!).

- Taxable Brokerage Accounts: Move these into the trust’s name to ensure seamless management.

Note: Be careful with 401ks and IRAs. These usually stay in your name for tax reasons, but you should name the trust as a secondary beneficiary after your spouse.

Timeline: When to Get This Done

I always recommend my clients aim to have their trust signed and notarized by the 32nd week of pregnancy. Why? Because after that, the ‘pregnancy brain’ gets real, the physical discomfort increases, and your focus shifts entirely to the nursery and the birth. You want this ‘off your plate’ so you can enter your ‘Golden Month’ of postpartum recovery with zero legal anxieties.

| Phase | Action Item | Time Estimate |

|---|---|---|

| Research | Identify 3 local estate planning attorneys or a reputable online service. | 1 Week |

| Decision | Choose your Guardian and Trustee (and backups!). | 1-2 Weeks |

| Drafting | Attorney prepares the documents based on your wishes. | 2-4 Weeks |

| Signing | Notarize the documents (The ‘Champagne’ moment!). | 1 Day |

| Funding | Transfer titles and update beneficiaries. | 2-4 Weeks |

Conclusion

Peace of Mind: The Greatest Baby Gift

Mama, I know that talking about trusts and wills feels heavy when you’re literally carrying the weight of a new life. But there is a profound sense of peace that comes when you click that binder shut and know that your baby is protected. You are doing the hard, invisible work of motherhood before your little one even arrives. You are building a fortress around their future.

By choosing a Revocable Living Trust over a simple will, you are choosing privacy over publicity, speed over bureaucracy, and wisdom over a random 18th-birthday windfall. You are giving your child—and their future guardians—the gift of a clear path forward during a difficult time. Now, take a deep breath, rub that beautiful belly, and know that you are doing an incredible job. Your ‘nest’ is officially secure.