Why New Parents Need Life Insurance (And How Much to Get)

Welcome to the Ultimate Act of Nesting, Mama

Let us take a deep, grounding breath together. In through the nose, out through the mouth. If you are here, you are likely in the beautiful, chaotic, and sometimes overwhelming season of preparing for a new baby. You are probably washing tiny onesies in gentle detergent, researching the safest car seats, and organizing the nursery closet by size and season. We call this nesting, and it is a primal, beautiful instinct to prepare a safe haven for your little one. But today, we are going to talk about a different kind of nesting. It is not as visually satisfying as folding muslin swaddles, but it is arguably the most profound act of love and protection you can offer your growing family: securing life insurance.

As a maternal wellness guide and doula, I hold space for all the emotions that come with pregnancy and postpartum. I know that talking about life insurance feels heavy. It requires us to look at the ‘what ifs’ during a time when we only want to focus on new life, first giggles, and sweet baby smell. It is completely normal to feel a wave of anxiety or resistance when this topic comes up. Your body is busy growing a human; your mind wants to protect that human from every conceivable danger. Thinking about a future where you or your partner might not be there goes against every maternal instinct we have.

Take a gentle breath, sister. Securing life insurance is not about inviting worry into your space; it is about evicting it. It is about building an invisible, unbreakable safety net beneath your family so that you can sleep a little sounder at night.

In this comprehensive, sisterly guide, we are going to demystify life insurance. We will walk through exactly why new parents need it, break down the confusing industry jargon into plain English, and show you exactly how to calculate the coverage you need. Whether you are the primary breadwinner, a partner sharing the financial load, or a mother planning to pour your heart into full-time caregiving at home, your presence has immense value. Let us gently unpack this together, step by step, so you can check this off your list and get back to the joyful parts of nesting.

Why Life Insurance is Essential for Growing Families

The Emotional and Practical Reality

When it is just you and your partner, life insurance might feel like an optional adulting milestone, something you will get around to ‘someday.’ But the moment you see those two pink lines, the calculus of your life shifts entirely. Suddenly, there is a tiny, vulnerable person who relies on you for absolutely everything: food, shelter, education, and love. Life insurance is the financial translation of that love. If the unthinkable were to happen, the emotional devastation would be world-shattering for your family. The purpose of life insurance is to ensure that financial devastation does not compound that grief. It provides the surviving parent or guardian with the ultimate gift: time and breathing room.

What Exactly Does Life Insurance Cover?

Many new parents mistakenly believe that life insurance is only meant to cover funeral expenses. While it certainly can do that, its primary purpose for young families is income replacement and lifestyle maintenance. Here is what a well-planned policy actually protects:

- Daily Living Expenses: Groceries, utility bills, clothing, and transportation.

- Housing Security: Paying off the remaining mortgage or guaranteeing rent money for years to come, so your family never has to uproot during a crisis.

- Childcare and Education: Covering the staggering costs of daycare, nannies, and eventually, college tuition.

- Time to Grieve: Allowing the surviving partner to take extended time off work to mourn, heal, and be present for the children without the immediate panic of returning to the office to pay the bills.

Think of life insurance as a love letter to your family’s future. It says, ‘Even if I cannot physically be here to provide for you, I have made sure you will always be warm, safe, and cared for.’

Term vs. Whole Life Insurance: Demystifying the Jargon

Keeping It Simple for Sleep-Deprived Parents

If you have started researching life insurance, you have probably been bombarded with complex terms, aggressive sales pitches, and confusing charts. Let us clear the noise. As a doula cuts through medical jargon in the delivery room, I am going to cut through the financial jargon right now. There are generally two main types of life insurance you will encounter: Term Life Insurance and Whole Life Insurance.

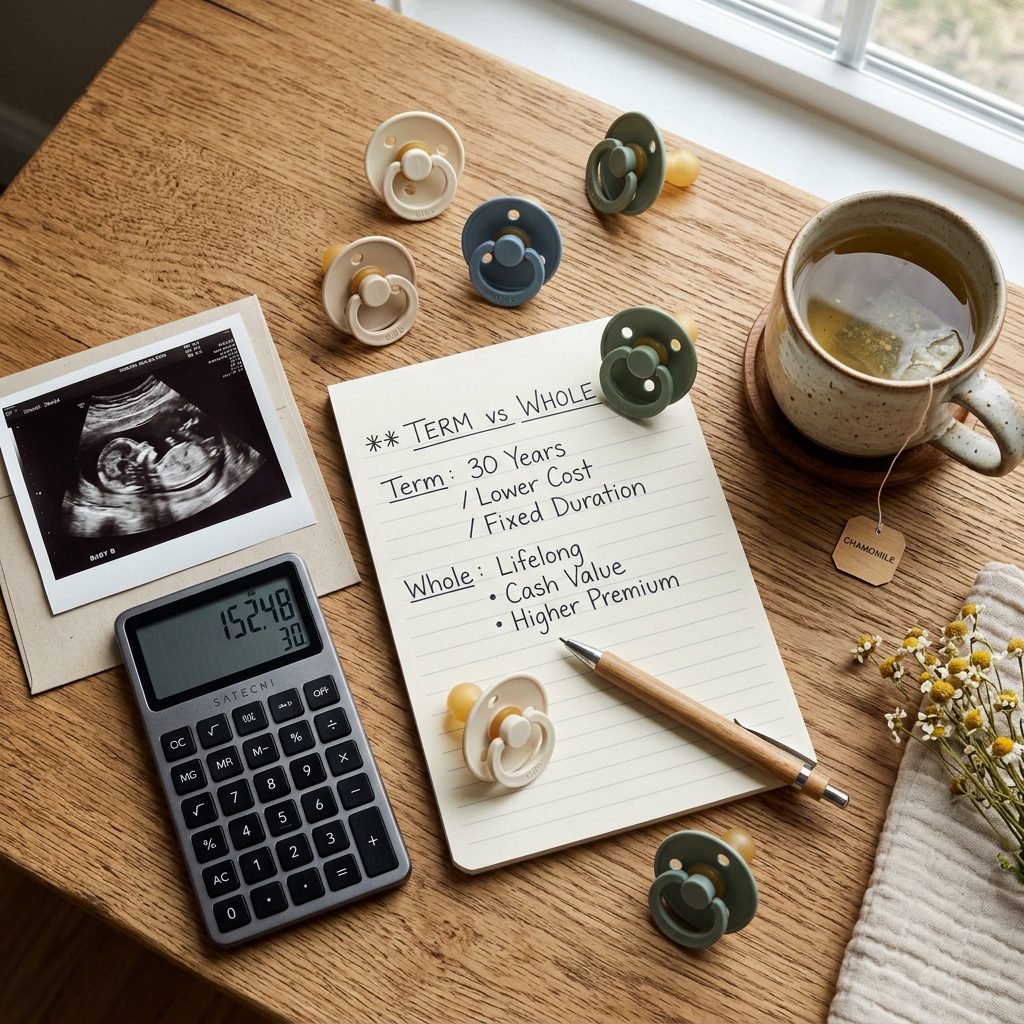

Term Life Insurance: The Gold Standard for New Parents

For the vast majority of young, growing families, Term Life Insurance is the exact right choice. Term insurance covers you for a specific ‘term’ or period of time—usually 10, 20, or 30 years. You pay a set monthly premium, and if you pass away during that term, your family receives the payout. If you outlive the policy (which is the goal!), the policy simply expires.

- Why it works: It is incredibly affordable. You only pay for insurance during the years you actually need it—the years when your children are dependent on you, your mortgage is highest, and your savings are still growing.

- The Doula Analogy: Think of Term Life Insurance like renting a heavy-duty breast pump. You only need it for a specific season of your life. Once your baby is weaned, you do not need to keep paying for it.

Whole Life Insurance: The Expensive Alternative

Whole Life Insurance (a type of permanent life insurance) covers you for your entire life, as long as you pay the premiums. It also includes a ‘cash value’ savings component that grows over time. While this sounds great in theory, the premiums are often 5 to 15 times more expensive than term life insurance for the exact same death benefit.

- The Reality Check: Because Whole Life is so expensive, many families end up buying less coverage than they actually need just to afford the monthly payment. As a new parent, your priority is maximum protection right now, not a complex investment vehicle.

Side-by-Side Comparison

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Duration | Specific period (e.g., 20 or 30 years) | Entire lifetime |

| Cost | Highly affordable (often $20-$40/month) | Very expensive (often $200-$500+/month) |

| Cash Value | None. Pure protection. | Builds a small cash value over time. |

| Best For… | 99% of new parents needing maximum coverage on a budget. | High-net-worth individuals with complex estate planning needs. |

The DIME Method: Exactly How Much Coverage You Need

Calculating Your Family’s Safety Net

One of the most common questions I hear from expectant parents is, ‘How much coverage should we actually get?’ It is easy to just pull a number out of thin air, like $500,000, but that might not actually cover your family’s unique needs. To figure out your exact number, financial experts recommend a beautifully simple formula called the DIME Method. Let us break it down together.

- D – Debt and Final Expenses: Add up all your current debts (excluding your mortgage, we will get to that). This includes student loans, credit card balances, auto loans, and personal loans. Then, add an estimated $10,000 to $15,000 to cover funeral and final medical expenses. You do not want your grieving partner to inherit your student loan payments.

- I – Income Replacement: This is the largest chunk of your policy. The goal is to replace your income for the number of years your youngest child will need support (usually until they are 18 or out of college). A good rule of thumb is to take your current annual salary and multiply it by 10 to 15 years. If you make $70,000 a year, that is $700,000 to $1,050,000 in income replacement.

- M – Mortgage: Look at the remaining balance on your home mortgage. If you owe $300,000 on your house, add $300,000 to your total. The goal is to ensure your family can pay off the house completely, removing their largest monthly living expense and securing their physical sanctuary.

- E – Education: If you want to cover your children’s future college tuition, add an estimate for each child. Currently, a four-year public university averages about $100,000 per child (including room and board). Add this to your total if funding their education is a priority.

Let us look at a real-life example for a new mama making $60,000 a year:

| DIME Category | Estimated Amount | Notes |

|---|---|---|

| Debt & Final Expenses | $35,000 | $20k student loans + $15k final expenses |

| Income Replacement | $600,000 | $60,000 salary x 10 years |

| Mortgage Balance | $250,000 | To pay off the family home |

| Education (1 Child) | $100,000 | Estimated 4-year state college cost |

| Total Coverage Needed | $985,000 | Round up to a $1,000,000 Term Policy |

Seeing a number like one million dollars can feel shocking at first! But take a deep breath. Because term life insurance is so affordable, a healthy 30-year-old woman can often secure a 20-year, $1,000,000 term policy for just $30 to $50 a month. That is roughly the cost of one package of premium diapers, but it buys a million dollars of peace of mind.

But I am a Stay-at-Home Mom! (Why Your Labor is Invaluable)

Validating the Invisible Work of Motherhood

This is a section I am incredibly passionate about. So often, I sit with expectant mothers who plan to leave the traditional workforce to stay home with their babies. When the topic of life insurance comes up, they gently wave it off, saying, ‘Oh, we only need a policy for my partner. I do not bring in an income, so we do not need to replace my salary.’ Mama, let me hold your hands and tell you this with absolute certainty: Your labor has immense, staggering financial value.

Being a stay-at-home parent is not just a role; it is a compilation of multiple full-time jobs. You are the private chef, the day-and-night childcare provider, the house manager, the chauffeur, the tutor, and the personal assistant. If you were suddenly gone, your partner would not only be navigating unimaginable grief as a now-single parent, but they would also have to instantly hire people to do all the things you did effortlessly out of love.

The True Cost of Replacing a Stay-at-Home Parent

Let us look at the hard numbers. According to recent studies that calculate the market value of the various jobs a stay-at-home parent performs, the equivalent salary is estimated to be over $160,000 per year. If your partner had to continue working their full-time job to support the family, they would immediately need to pay for:

- Full-Time Childcare or a Nanny: $20,000 to $40,000+ per year, depending on your location.

- Housecleaning Services: $3,000 to $5,000+ per year.

- Meal Delivery or a Cook: $5,000 to $10,000+ per year.

- Transportation and Errand Services: Additional thousands per year.

Without a life insurance policy on the stay-at-home parent, the surviving partner is often forced into an impossible corner. They either have to take on massive debt to pay for childcare, or they have to quit their own job to care for the children, instantly losing the family’s only source of income. Stay-at-home parents need life insurance just as much as the primary breadwinner. I recommend a minimum of a $500,000 to $750,000 term policy for the caregiving parent to ensure the surviving partner can afford the support they will desperately need.

How to Talk to Your Partner About Life Insurance (Without the Panic)

Guiding the Conversation with Love and Logic

Bringing up life insurance can feel awkward. It is the ultimate mood-killer when you are supposed to be celebrating new life. Depending on your partner’s personality, they might be avoidant, anxious, or just plain dismissive because ‘we are young and healthy.’ As a doula, I teach couples how to communicate through the intense waves of labor. We can use those same communication tools here: grounding language, validation, and a focus on the shared goal of protecting the baby.

Scripts for Different Partner Dynamics

Here are a few gentle, copy-and-paste scripts you can use to initiate this conversation, depending on how your partner usually handles financial discussions:

For the Avoidant/Anxious Partner:

‘Hey love, I know this is a really heavy topic, and honestly, it makes me anxious to even think about it. But as part of our nesting and getting ready for the baby, I want to make sure we are both protected no matter what happens. Can we spend 20 minutes this Sunday looking at term life insurance quotes together? Once it is done, we never have to think about it again, and I will sleep so much better knowing our baby is safe.’

For the Budget-Conscious Partner:

‘I was reading today about how affordable term life insurance is for people our age. I know we are trying to save money for the baby, but I found out we could get a million dollars in coverage for less than what we spend on takeout each month. It feels like a really smart financial move to lock in a low rate while we are young and healthy. Can we look at the budget and carve out $50 a month for this?’

For the ‘We Have Plenty of Time’ Partner:

‘I love how optimistic we are about our future, and I am planning on us growing old and gray together. But pregnancy has made me realize how fragile life can be. Getting life insurance right now is just a backup parachute. We do not plan on the plane crashing, but I want to know the parachute is packed before the baby gets here. Let us just get some free quotes today to see what our options are.’

Set a specific date and time to sit down with a cup of tea, your laptops, and an open heart. Do not try to have this conversation in passing while rushing out the door. Treat it with the sacred importance it deserves.

When and How to Apply: A Step-by-Step Guide

Timing is Everything

The absolute best time to buy life insurance is right now. The younger and healthier you are, the lower your monthly premiums will be for the entire duration of the term. However, if you are currently pregnant, there are a few nuances to keep in mind.

Pregnancy can sometimes temporarily alter your health metrics. Your weight increases, your blood pressure might fluctuate, and you might develop temporary conditions like gestational diabetes. Because many life insurance policies require a brief medical exam (where a nurse comes to your home to check your vitals and take a blood sample), these pregnancy-related changes can sometimes result in slightly higher premiums. The sweet spot for applying during pregnancy is often the late first trimester or early second trimester, before significant weight gain or late-stage pregnancy complications arise.

The Step-by-Step Application Process

- Calculate Your Needs: Sit down with your partner and use the DIME method (detailed above) to figure out exactly how much coverage you both need. Remember, you should each have your own separate policy.

- Shop Around for Quotes: Do not just go with the first company you find. Use an online broker or aggregator (like Policygenius or Haven Life) to compare quotes from multiple highly-rated insurance carriers simultaneously.

- Choose Your Term Length: Most parents choose a 20-year or 30-year term. A 20-year term will cover you until your newborn is in college. A 30-year term will cover you until they are well into adulthood.

- Submit the Application: You will answer a detailed questionnaire about your medical history, your family’s medical history, and your lifestyle (e.g., if you participate in extreme sports or use tobacco). Always be 100% honest. Lying on an application can invalidate your policy later.

- Take the Medical Exam (If Required): Many modern companies now offer ‘no-exam’ policies that use algorithms to approve you instantly based on your medical records. If an exam is required, a technician will come to your house for a free, 15-minute checkup.

- Sign and Pay: Once approved, you will sign the final documents and make your first premium payment. Your coverage begins immediately upon that first payment.

Conclusion

You Are Doing an Amazing Job, Mama

We have covered a lot of heavy, deeply emotional ground today. If you are feeling a little overwhelmed, I want you to place a hand on your belly or your heart and take another deep breath. You are doing exactly what a good mother does: you are looking ahead, anticipating needs, and fiercely protecting your family. Securing life insurance is not a fun baby shower topic, and it does not result in a cute nursery photo for Instagram. But it is the quiet, steadfast foundation of your family’s financial security.

By taking the time to understand term vs. whole life, calculating your DIME numbers, validating the immense worth of stay-at-home parenting, and having brave conversations with your partner, you are actively building a wall of protection around your child’s future. You are ensuring that their life will always be filled with the warmth, stability, and opportunity you dream of for them, no matter what twists and turns life takes.

So, pour yourself another cup of warm tea, pull up those online quotes, and check this massive task off your nesting to-do list. Once it is done, you can file the paperwork away in a drawer, take a deep breath of relief, and get back to the joyful, beautiful work of preparing to meet your baby. You have got this, sister.